Sukanya Samriddhi Yojana (SSY) – Complete Guide for Your Daughter’s Future

Most parents open a bank account for their daughter and never compare it against a scheme built for exactly this purpose. The Sukanya Samriddhi Yojana (SSY) still pays more than any other government-backed savings option in India: 8.2% per annum, tax-free at every stage. That gap compounds into lakhs over 21 years.

This guide walks through eligibility, deposit rules, the current interest rate, what your money grows to, tax treatment under both regimes, how SSY stacks up against PPF and fixed deposits, and the steps to open an account.

Key Takeaways

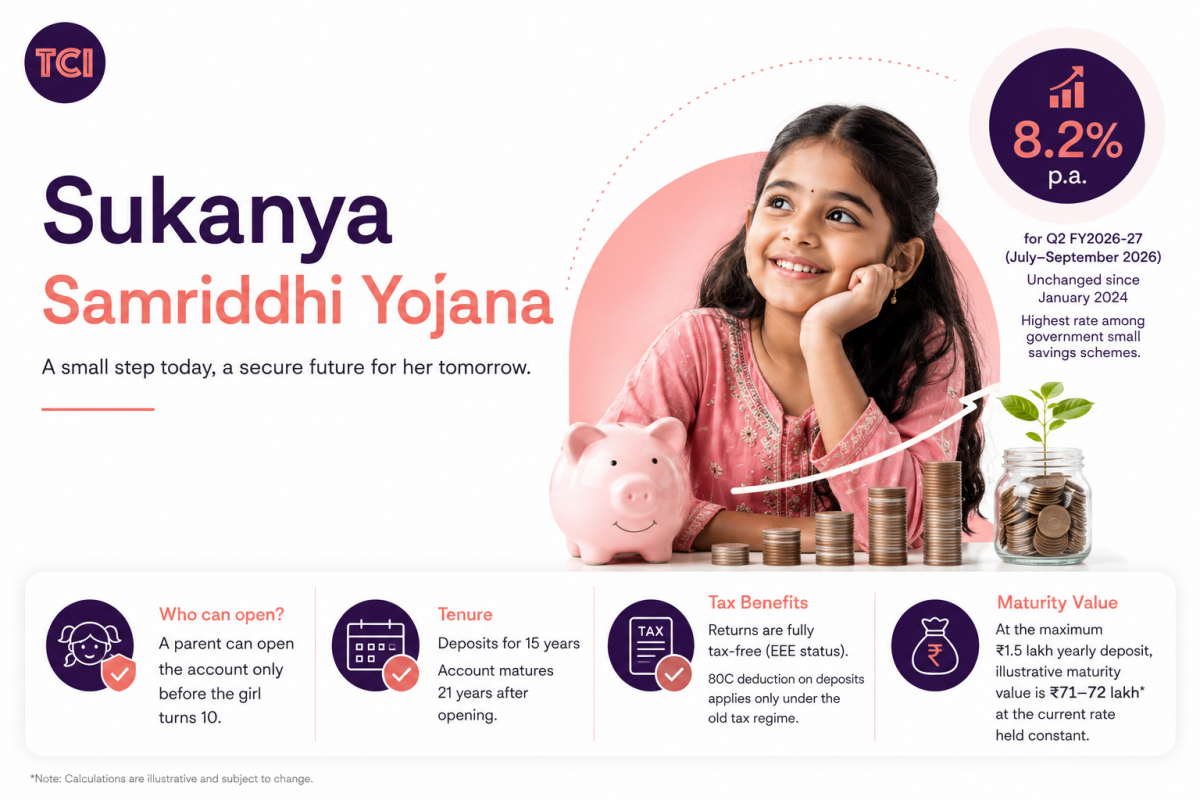

- SSY pays 8.2% p.a. for Q2 FY2026-27 (July–September 2026), unchanged since January 2024, the highest rate among government small savings schemes.

- A parent can open the account only before the girl turns 10; deposits run for 15 years, and the account matures 21 years after opening.

- Returns are fully tax-free (EEE status), but the Section 80C deduction on deposits applies only under the old tax regime.

- At the maximum ₹1.5 lakh yearly deposit, illustrative maturity value is ₹71–72 lakh at the current rate held constant.

Table of Contents

What Is Sukanya Samriddhi Yojana?

The Government of India launched Sukanya Samriddhi Yojana in January 2015 under the Beti Bachao Beti Padhao campaign, aimed at giving parents of daughters a guaranteed, tax-free place to build a corpus for education and marriage. The Ministry of Finance runs the scheme; India Post and authorised banks sell it.

The appeal isn’t complicated. SSY carries a sovereign guarantee, so the principal stays protected, and the returns beat most fixed-income options available to retail investors. There’s no market risk and no credit risk. Nobody makes a fund-manager judgment call on your behalf, only a fixed government-notified rate, reviewed every quarter.

As of November 2024, the scheme had over 4.2 crore subscribers, per Ministry of Finance data cited by Upstox’s 10-year retrospective on SSY. That scale shows how mainstream this account has become for Indian families.

Who Is Eligible to Open an SSY Account?

A parent or legal guardian can open an SSY account for a girl child below 10 years of age, at any post office or authorised bank. Miss that window and there’s no workaround: no provision exists to open an account for a girl who’s already 10 or older.

Family-level limits also apply. A family can open a maximum of two SSY accounts, one for each girl child, with a third allowed only in the case of twins or triplets (Wikipedia, Sukanya Samriddhi Account, 2026; Smart Paisa, 2026).

Can NRIs or a girl above 10 open an account?

No, on both counts. Per Policybazaar’s 2026 SSY guide, the girl child must be a resident Indian at the time of account opening. If she becomes a non-resident or non-citizen afterward, interest stops accruing from that date and the account must be closed. Families who relocate abroad after opening the account run into this most often, so check residency status before assuming the account continues as-is.

Read: PM Jeevan Jyoti Bima Yojana (PMJJBY): ₹436/Year Life Insurance for All Indians

How Much Can You Deposit in SSY?

Deposit rules are simple on paper but trip up a lot of parents in practice. The minimum deposit to keep an SSY account active is ₹250 per year, and the maximum is ₹1,50,000 per financial year (Wikipedia, Sukanya Samriddhi Account, 2026). Deposit above that ceiling and the bank refunds the excess without paying interest on it, so there’s no benefit to over-depositing in a single year.

You don’t need to deposit every year forever, either. Per StableInvestor’s 2026 SSY guide, deposits are required only for the first 15 years from account opening; after that, the balance keeps earning interest until the account completes 21 years. Skip a year within that 15-year window, though, and the bank marks the account discontinued. Reviving it means paying the missed year’s minimum deposit plus a ₹50 penalty (Wikipedia, Sukanya Samriddhi Account, 2026).

The 5th-day rule for interest calculation

Banks and post offices calculate SSY interest on the lowest balance held between the 5th and the last day of each month, per most calculator and post-office guides (a minority of sources cite the 10th day instead, so confirm the exact cutoff with your branch). Deposit after that cutoff and that month’s interest calculation misses your latest deposit. Over 15 years, this timing detail adds up to a noticeable difference in total interest earned.

What Is the Current SSY Interest Rate, and How Is It Set?

As of July 2026, StableInvestor’s rate tracker confirms the SSY interest rate remains at 8.2% per annum for Q2 FY2026-27 (July–September 2026), compounded annually and credited each March 31. That’s the 11th straight quarter at this level, going back to January 2024.

The government ties SSY and other small savings rates to G-Sec yields, per the Shyamala Gopinath Committee formula, and reviews them every quarter.

Per Business Today’s 10-year retrospective, the scheme launched at 9.1% in December 2014, rose to 9.2% for FY2015-16, then declined step by step to a low of 7.6% between April 2020 and March 2023, before recovering to 8.0% in 2023 and then 8.2% from January 2024 onward. Rates have moved with the broader interest-rate cycle, but SSY has stayed at or near the top of the small-savings pile throughout.

Most calculators gloss over one detail: because the rate resets every quarter, no maturity figure you see online, including the ones in this article, is a guarantee. They’re all snapshots based on today’s rate held constant for 21 years, which has never happened in the scheme’s history. Plan around a range, not a single number.

Read: UDAN Scheme – How India’s Regional Air Connectivity Plan Works for Tier-2 & Tier-3 Cities

How Much Will Your Daughter Get at Maturity?

Run the numbers at today’s 8.2% rate: depositing ₹60,000 a year (₹5,000/month) for 15 years, then letting the balance sit for the remaining 6 years, produces an illustrative maturity value of ₹28.7 lakh on a total investment of ₹9 lakh.

The account matures 21 years from the date it was opened, not from the girl’s birth date and not when she turns 21. Open the account the day she’s born and you get the full 21-year compounding runway. Open it when she’s 8, and the account still runs 21 years from that later start date, maturing when she’s 29.

Three deposit scenarios, compounded at 8.2%

At the maximum deposit level, the numbers line up with what other calculators show for a maxed-out account. Opening SSY at birth and investing the maximum amount for 15 years at 8.2% produces a maturity figure with a large share made up of tax-free interest. In our calculation, ₹49.3 lakh of the ₹71.8 lakh total is compounding gain, not principal.

What Are the Tax Benefits of Sukanya Samriddhi Yojana?

SSY carries EEE status (Exempt-Exempt-Exempt) under the Income Tax Act, 1961, the same tax treatment as PPF. That makes it one of the most tax-efficient long-term savings instruments available to Indian investors in 2026.

That means three separate exemptions stack together: the deposit qualifies for a deduction, the interest earned isn’t taxed, and the maturity payout isn’t taxed either.

SSY vs. the New Tax Regime: Which Wins?

This is where families get tripped up in 2026. The Section 80C deduction is available only under the old tax regime; the new tax regime, default from FY 2024-25, doesn’t allow it. Interest and the maturity amount stay tax-free under both regimes.

For a parent in the 30% tax bracket investing ₹1,50,000 per year, the Section 80C deduction alone saves ₹46,800 in tax every year for 15 years under the old regime. The new regime drops that upfront saving, but the account still delivers a tax-free maturity corpus. The decision comes down to whether the 80C deduction is worth more to you than the simplicity of the new regime’s flat structure.

SSY vs PPF vs FD vs Mutual Funds: Which Is Best for Your Daughter?

For a girl-child-specific, capital-guaranteed goal, SSY is hard to beat on raw rate. At 8.2%, SSY beats PPF’s 7.1% by 1.1 percentage points (StableInvestor, July 2026 small savings rate roundup), and most bank FDs sit in the 6.5–7.5% range. Rate alone isn’t the whole comparison: liquidity and flexibility matter as much for a 21-year commitment.

Comparison Table: SSY vs PPF vs FD vs Equity SIP

| Feature | SSY | PPF | Bank FD | Equity SIP |

|---|---|---|---|---|

| Current rate | 8.2% p.a. (fixed, govt-set) | 7.1% p.a. | ~6.5–7.5% p.a. | No fixed rate; market-linked |

| Risk | None (sovereign) | None (sovereign) | Low (bank-dependent) | Market risk |

| Tax treatment | EEE | EEE | Taxable interest | LTCG tax on gains above threshold |

| Eligibility | Girl child, before age 10 | Any resident individual | Anyone | Anyone |

| Liquidity | Locked till maturity, partial withdrawal at 18 | Partial withdrawal after year 7 | Flexible tenures | Fully liquid (subject to exit load) |

| Best for | Dedicated daughter’s education/marriage goal | General long-term tax-saving | Short-to-medium term parking | Long-term growth, higher risk tolerance |

PPF offers more flexibility for a family that isn’t sure the money is only for one daughter’s goals, since it isn’t restricted by gender or a 10-year opening window. Equity SIPs have delivered higher average long-term returns than any fixed-income instrument, but that comes with real volatility. A poor sequence of market years right before your daughter needs the money can hurt.

Running the same 15-year, ₹60,000/year contribution through SSY versus a PPF at 7.1% shows a real gap: SSY’s illustrative ₹28.7 lakh outcome comes in close to ₹2 lakh higher than the equivalent PPF corpus, from the extra 1.1 percentage points compounding over two decades.

Many families split the difference: max out SSY for the guaranteed portion of the goal, and run a smaller equity SIP alongside it for long-term growth, accepting some risk on that second layer.

How to Open an SSY Account: Documents & Step-by-Step Process

Opening the account is straightforward and takes one branch visit in most cases. You’ll need the girl child’s birth certificate, identity and address proof for the parent or guardian, and passport-size photographs.

Step-by-step:

- Visit any post office or an authorised bank branch (SBI, ICICI, HDFC, Axis, and India Post Payments Bank are among the most common).

- Fill out the SSY account opening form with the girl child’s and guardian’s details.

- Submit KYC documents along with the birth certificate.

- Make the initial deposit: minimum ₹250.

- Collect the passbook and set a yearly deposit reminder so the account never lapses into discontinued status.

HDFC Bank, Axis Bank, and India Post Payments Bank offer online SSY account opening for existing customers, though most other banks and all post offices still require an in-person visit for the first deposit. Subsequent yearly deposits can be made online once the account exists, in most cases.

Withdrawal, partial withdrawal, and premature closure rules

Up to 50% of the balance at the end of the preceding financial year can be withdrawn for the girl’s higher education, subject to age and documentation conditions. Beyond that, the account matures 21 years from opening, or when the girl marries after age 18, whichever comes first.

You can also close the account early on compassionate grounds: the account holder’s death, a life-threatening medical condition, or the guardian’s inability to continue operating the account, each requiring separate supporting documentation at the bank or post office.

Frequently Asked Questions

What is the current Sukanya Samriddhi Yojana interest rate?

The SSY interest rate for Q2 FY2026-27 (July–September 2026) is 8.2% per annum, compounded annually. It has held at this level for 11 consecutive quarters since January 2024, per StableInvestor’s rate archive.

Can I open more than one SSY account for the same daughter?

No. A girl child can hold only one SSY account, and a family can open a maximum of two accounts, one per daughter, with a third permitted only for twins or triplets in specific birth-order situations.

What happens if I miss a yearly deposit?

The bank marks the account discontinued if the ₹250 minimum isn’t deposited in a given year. Reviving it requires paying the shortfall for each missed year plus a ₹50 penalty per missed year, at the bank or post office where the account is held.

Can NRIs invest in Sukanya Samriddhi Yojana?

No. The girl child must be a resident Indian at account opening, and if she or the family’s residency status changes to non-resident afterward, interest stops accruing from that date and the account must be closed under current rules.

Is the SSY maturity amount taxable?

No. The maturity amount is tax-free under SSY’s EEE (Exempt-Exempt-Exempt) status, and this holds true regardless of whether you file under the old or the new tax regime.

Conclusion

SSY remains the highest-paying government-backed savings option for a girl child in 2026, with a guaranteed 8.2% rate and tax-free returns at every stage. The catch is timing: you can only open the account before your daughter turns 10, and the earlier you start, the longer the money compounds.

If you’re still deciding, run your own numbers through an SSY calculator before committing to a deposit amount, and visit your nearest post office or bank branch to open the account well before that 10-year age cutoff.

Interesting Reads

- Which Government Schemes Provide Free or Subsidized Education for College Students?

- Mission Indradhanush: India’s Free Vaccination Program for Children and Pregnant Women

- PM Kaushal Vikas Yojana (PMKVY)- Free Skill Training, Benefits, and How to Apply

- List Of Central and State Government Schemes for Women’s Self-Help Groups in India

Sources

- StableInvestor, “Sukanya Samriddhi Yojana Interest Rate History (2026),” retrieved 2026-07-09, https://stableinvestor.com/2019/06/sukanya-samriddhi-yojana-interest-rates.html

- Policybazaar, “Sukanya Samriddhi Yojana Interest Rate FY 2026-27,” retrieved 2026-07-09, https://www.policybazaar.com/life-insurance/child-plans/news/sukanya-samriddhi-yojana-interest-rate/

- BusinessToday, “Sukanya Samriddhi Yojana: In 10 years, interest rates swinged from 9.1% to 8.2%,” retrieved 2026-07-09, https://www.businesstoday.in/personal-finance/investment/story/sukanya-samriddhi-yojana-in-10-years-interest-rates-swinged-from-91-to-82-check-details-462025-2025-01-25

- Upstox, “Sukanya Samriddhi Yojana turns 10: How the SSY interest rate moved in 10 years,” retrieved 2026-07-09, https://upstox.com/news/personal-finance/investing/sukanya-samriddhi-yojana-how-ssy-interest-rate-moved-up-and-down-from-9-2-to-8-2-in-10-years/article-141843/

- Wikipedia, “Sukanya Samriddhi Account,” retrieved 2026-07-09, https://en.wikipedia.org/wiki/Sukanya_Samriddhi_Account

- Smart Paisa, “Sukanya Samriddhi Yojana Scheme Account,” retrieved 2026-07-09, https://www.smartpaisa.in/sukanya-samriddhi-yojana-scheme-account-interest-rate-history/

- Freefincal, “Sukanya Samriddhi Yojana Interest Rate History 2015 to Present,” retrieved 2026-07-09, https://freefincal.com/sukanya-samriddhi-yojana-interest-rate-history-2015-to-present/

- Holistic Investment, “Interest Rate of Sukanya Samriddhi Yojana (SSY) 2015–2025,” retrieved 2026-07-09, https://www.holisticinvestment.in/current-latest-historical-interest-rate-sukanya-samriddhi-yojana/

This article is for informational purposes only and does not constitute financial advice. Interest rates are revised quarterly by the Ministry of Finance; verify the current rate and rules at your nearest post office or bank before investing.