Mutual Funds For NRIs In India: Where to Invest in 2026

| Quick Summary: Mutual Funds For NRIs In India (2026) NRIs (Non-Resident Indians) can legally invest in Indian mutual funds under FEMA regulations. Investments are made through NRE or NRO bank accounts. Popular fund categories include equity, debt, hybrid, and ELSS (tax-saving) funds. KYC compliance and FATCA/CRS declarations are mandatory. US- and Canada-based NRIs face some restrictions due to FATCA compliance. Returns are subject to Indian capital gains tax, with TDS applied at source. Top fund houses accepting NRI investments include SBI MF, HDFC MF, ICICI Prudential MF, Nippon India MF, and Mirae Asset MF. |

If you are an NRI (Non-Resident Indian) thinking about growing your money back home, mutual funds for NRIs are one of the smartest options available to you in 2026. India’s mutual fund industry crossed ₹66 lakh crore in assets under management (AUM) in early 2025, and it continues to grow. NRIs are a big part of that story.

This guide covers everything you need to know: which funds to pick, how to invest from abroad, what documents you need, how you get taxed, and which fund houses welcome NRI investors. Whether you live in the US, UK, UAE, or Australia, this article is your complete starting point.

Read: DTAA India for NRIs – How India’s Double Taxation Avoidance Agreement Works

Table of Contents

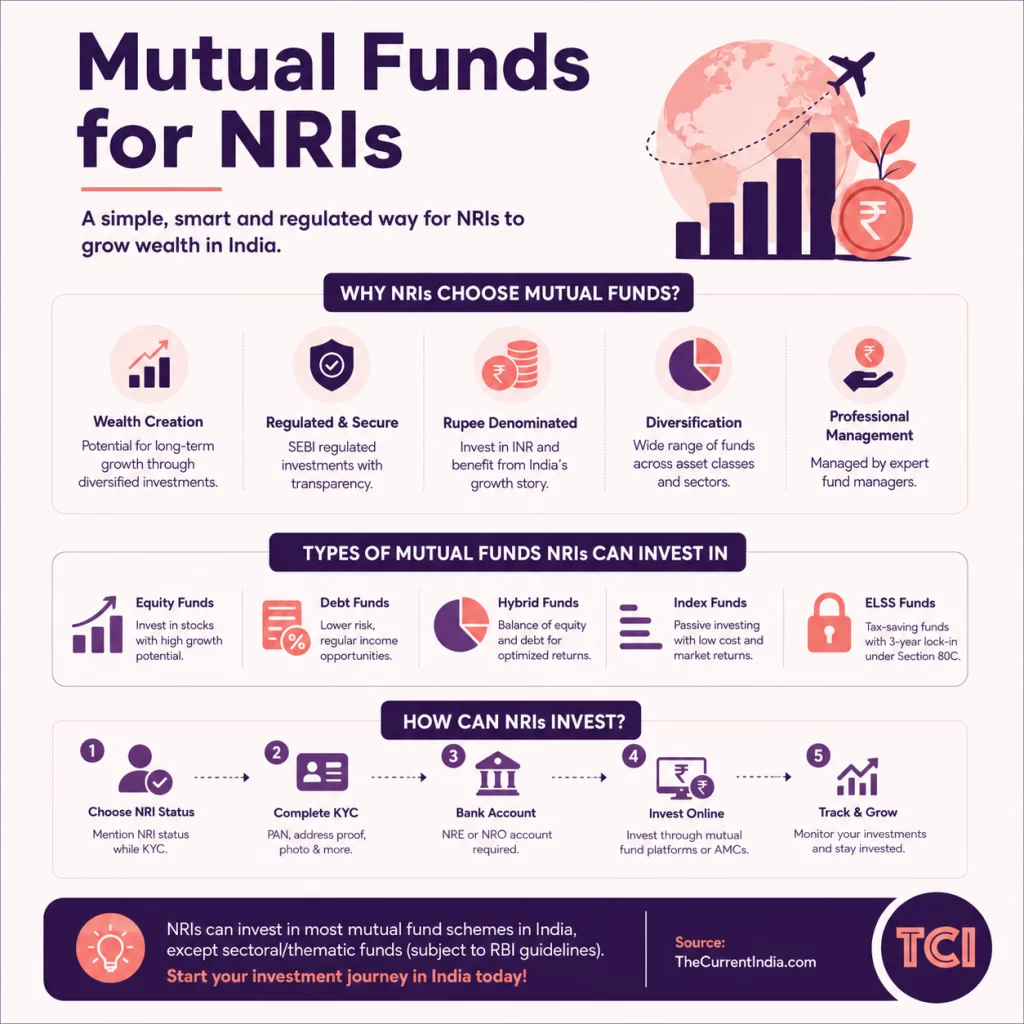

What Are Mutual Funds For NRIs?

Mutual funds for NRIs work exactly the same way as they do for resident Indians. A fund house (also called an AMC, or Asset Management Company) pools money from many investors and invests it in stocks, bonds, or a mix of both. A professional fund manager makes all the investment decisions.

As an NRI, you invest in these funds using money from your Indian bank account, either an NRE (Non-Resident External) or NRO (Non-Resident Ordinary) account. The Securities and Exchange Board of India (SEBI) and the Foreign Exchange Management Act (FEMA) govern NRI investments in mutual funds.

Can NRIs Invest in Mutual Funds in India?

Yes, NRIs can legally invest in Indian mutual funds. FEMA regulations allow NRIs to invest on a repatriable or non-repatriable basis depending on the bank account they use.

| Account Type | What It Means for NRIs |

|---|---|

| NRE Account | Investments are fully repatriable. You can take your money and returns back to your country of residence without restriction. |

| NRO Account | Investments are non-repatriable up to USD 1 million per financial year. Good for income earned in India (rent, dividends, etc.). |

Important: NRIs from the USA and Canada face additional restrictions. Many Indian fund houses do not accept investments from US/Canada-based NRIs due to FATCA (Foreign Account Tax Compliance Act) compliance costs. However, some AMCs like SBI Mutual Fund, UTI Mutual Fund, ICICI Prudential, and Nippon India do accept US/Canada NRI investors with proper FATCA declarations.

Read: Health Insurance for NRIs: Comparison

Types of Mutual Funds NRIs Can Invest In

NRIs can invest in almost all categories of mutual funds that are available to resident Indians. Here is a quick breakdown:

1. Equity Mutual Funds

These funds invest mainly in stocks. They carry higher risk but also offer higher potential returns over the long term (5 years or more). Subcategories include:

- Large Cap Funds: Invest in India’s top 100 companies by market capitalization. Stable and less volatile.

- Mid Cap Funds: Invest in companies ranked 101-250. Higher growth potential but more volatile.

- Small Cap Funds: Invest in companies ranked below 250. High risk, high reward.

- Flexi Cap / Multi Cap Funds: Fund manager can move money across large, mid, and small cap as market conditions change.

2. Debt Mutual Funds

These funds invest in government bonds, corporate bonds, and money market instruments. They are lower risk and suitable for capital preservation and short- to medium-term goals.

3. Hybrid Mutual Funds

Hybrid funds invest in both equity and debt. They offer a balance of growth and stability. Balanced Advantage Funds and Aggressive Hybrid Funds are popular choices.

4. ELSS (Equity Linked Savings Scheme)

ELSS funds are tax-saving mutual funds. Investments up to ₹1.5 lakh per year qualify for deduction under Section 80C of the Income Tax Act. They come with a 3-year lock-in period. These are among the most popular mutual funds for NRIs who have taxable income in India.

5. Index Funds and ETFs

Index funds track a market index like Nifty 50 or Sensex. They are passively managed, have low costs, and are excellent for long-term wealth building. Exchange Traded Funds (ETFs) work similarly but trade on the stock exchange like shares.

What Are the Best Indian Mutual Fund Schemes for NRIs?

The right fund depends on your goals, risk appetite, and investment horizon. Below is a curated, data-driven comparison of top-rated mutual fund schemes that accept NRI investments in 2026. Returns are approximate trailing 3-year figures based on historical performance and should not be treated as guaranteed.

| Fund Name | Category | 3-Yr Return (Approx.) | Risk Level | NRI-Friendly? |

| Mirae Asset Large Cap Fund | Large Cap Equity | ~14% p.a. | Moderate | Yes |

| SBI Bluechip Fund | Large Cap Equity | ~13% p.a. | Moderate | Yes |

| HDFC Mid-Cap Opportunities Fund | Mid Cap Equity | ~22% p.a. | High | Yes |

| Nippon India Small Cap Fund | Small Cap Equity | ~28% p.a. | Very High | Yes |

| ICICI Pru Equity & Debt Fund | Hybrid (Aggressive) | ~16% p.a. | Moderate-High | Yes |

| HDFC Balanced Advantage Fund | Dynamic Asset Alloc. | ~14% p.a. | Moderate | Yes |

| Axis ELSS Tax Saver Fund | ELSS (Tax-Saving) | ~15% p.a. | High | Yes |

| SBI ELSS Tax Saver Fund | ELSS (Tax-Saving) | ~16% p.a. | High | Yes |

| ICICI Pru Short Term Fund | Short Duration Debt | ~7% p.a. | Low-Moderate | Yes |

| Nippon India Liquid Fund | Liquid/Debt | ~6.5% p.a. | Low | Yes |

Note: Past returns do not guarantee future performance. Always check the fund’s latest factsheet and consult a SEBI-registered financial advisor before investing. Data sourced from AMFI India and respective AMC websites.

How to Choose the Right Fund as an NRI

Risk Tolerance: If you cannot handle large swings in portfolio value, stick with large cap or hybrid funds.

Investment Horizon: Equity funds work best over 5 years or more. Debt funds suit 1-3 year goals.

Repatriation Need: If you want to take money back abroad, invest via your NRE account for full repatriation.

Tax Efficiency: ELSS saves tax under Section 80C if you file Indian income tax returns.

Top Mutual Fund Companies Offering NRI Investment Services

Not all AMCs in India accept NRI investments, especially from NRIs based in the USA and Canada. Here are the top-rated mutual fund companies that are NRI-friendly:

- SBI Mutual Fund: India’s largest AMC by AUM. Accepts NRI investments including US- and Canada-based NRIs through its dedicated NRI investment portal.

- HDFC Mutual Fund: One of India’s most trusted AMCs. Accepts NRI investors from most countries. Does not accept US/Canada NRI investments directly in some schemes.

- ICICI Prudential Mutual Fund: Wide range of funds. Accepts NRI investors including those from the US and Canada with FATCA compliance.

- Nippon India Mutual Fund: Japanese-backed AMC. Has a robust NRI investment platform and accepts US/Canada NRI investments.

- Mirae Asset Mutual Fund: Known for consistent performance in equity funds. NRI-friendly across major geographies.

- UTI Mutual Fund: One of India’s oldest AMCs. Specifically set up for NRI investors in earlier years. Accepts US/Canada NRIs.

- Axis Mutual Fund: Strong ELSS and equity fund offerings. Accepts NRI investments from major geographies.

How Can NRIs Invest in Mutual Funds Through Online Platforms?

Investing in Indian mutual funds from abroad is easier than ever in 2026. You have multiple options:

Option 1: Invest Directly Through the AMC Website

Most major fund houses have online portals where NRIs can complete their KYC, link their NRE/NRO account, and start investing in minutes. Simply visit the AMC’s website, select the NRI investor section, and follow the steps.

Option 2: Use a SEBI-Registered Online Platform (MF Utility / MF Central)

MF Utility (MFU) and MF Central are government-backed platforms where you can manage investments across multiple fund houses from a single login. They support NRI investors and allow portfolio tracking, redemption, and switching online.

Option 3: Use a Third-Party Investment Platform

Apps and platforms like Kuvera, Groww, Zerodha Coin, and ETMONEY allow NRI investments in mutual funds with digital KYC. However, check each platform’s NRI eligibility, especially if you are based in the US or Canada.

Option 4: Invest Through an NRI-Focused Wealth Manager or Distributor

Several banks (HDFC Bank NRI Services, ICICI NRI Banking, SBI NRI Services) and wealth management firms offer assisted NRI investment services. They handle paperwork and compliance on your behalf.

Step-by-Step Process to Invest Online as an NRI

- Complete NRI KYC: Submit PAN, passport, overseas address proof, and photograph. In-person KYC (IPV) is often done via video call today.

- Link NRE/NRO Account: Add your Indian bank account details to the platform or AMC portal.

- Complete FATCA/CRS Declaration: This is mandatory. Declare your tax residency status.

- Choose Your Funds: Select funds based on your goals, risk profile, and investment horizon.

- Start a SIP or Lump Sum: Set up a Systematic Investment Plan (SIP) for regular monthly investments, or make a one-time lump sum investment.

- Track and Manage: Use the platform dashboard or CAMS/KFintech portals to track NAV, returns, and statements.

Documents Required for NRIs to Invest in Mutual Funds

Getting your documents ready before you start saves a lot of time. Here is the complete checklist:

| Document | Details |

| Passport | Valid passport copy (self-attested) |

| NRE / NRO Bank Account Proof | Statement or cancelled cheque from Indian bank |

| Overseas Address Proof | Utility bill, bank statement, or driving license from country of residence |

| PAN Card | Mandatory for all investments above ₹50,000 |

| Recent Photograph | Passport-size photo (for physical KYC) |

| FATCA / CRS Declaration | Self-declaration form for tax residency (US/Canada NRIs must comply strictly) |

| KYC Form | Completed and signed KYC application form |

Pro Tip: Many platforms now offer Video KYC (V-KYC), which lets you complete the verification process from your home abroad without visiting an Indian embassy or AMC branch.

Tax Implications for NRIs Investing in Indian Mutual Funds

Tax is one of the most important things NRIs need to understand before investing in Indian mutual funds. Here is a clear breakdown:

| Fund Type | Holding Period | Tax Rate | Surcharge/Cess |

| Equity Funds (STCG) | < 1 year | 15% | + 4% cess |

| Equity Funds (LTCG) | > 1 year | 10% on gains > ₹1 lakh | + 4% cess |

| Debt Funds (STCG) | < 3 years | As per income slab | + 4% cess |

| Debt Funds (LTCG) | > 3 years | 20% with indexation | + 4% cess |

| ELSS Funds (LTCG) | > 1 year (lock-in) | 10% on gains > ₹1 lakh | + 4% cess |

TDS (Tax Deducted at Source) for NRIs

Unlike resident Indians, NRIs have TDS deducted directly from their mutual fund redemption proceeds. The fund house deducts TDS before crediting money to your account. You can then claim a refund or credit when you file your Indian income tax return (ITR).

- TDS on Equity Fund STCG: 15%

- TDS on Equity Fund LTCG: 10%

- TDS on Debt Fund STCG: 30% (as per the highest slab for NRIs)

- TDS on Debt Fund LTCG: 20% with indexation

Double Taxation Avoidance Agreement (DTAA)

India has DTAA agreements with over 90 countries including the USA, UK, UAE, Canada, Australia, and Singapore. As an NRI, you may be able to reduce your tax liability by claiming DTAA benefits. Submit Form 10F and a Tax Residency Certificate from your country of residence to your fund house to claim lower TDS rates.

Important: Dividends from mutual funds are now taxable in the hands of the investor. TDS at 20% applies on dividend income for NRIs.

Benefits of Investing in Mutual Funds as an NRI

Why should you, as an NRI, choose mutual funds over other investment options like real estate, fixed deposits, or direct stock trading? Here are the key advantages:

- Rupee Appreciation Upside: If the Indian rupee strengthens against your country’s currency, your real returns increase. Historically, Indian equities have delivered strong long-term returns in absolute and relative terms.

- Portfolio Diversification: Mutual funds instantly give you exposure to dozens or hundreds of Indian companies across sectors. This reduces your risk compared to buying individual stocks.

- Professional Management: SEBI-registered fund managers with dedicated research teams actively manage your money (in actively managed funds). You do not need to track Indian markets daily from abroad.

- Systematic Investment Plans (SIPs): SIPs allow you to invest small amounts (as low as ₹500/month) regularly. This disciplines your savings and averages out market volatility over time.

- Liquidity: Open-ended mutual funds allow you to redeem your investment on any business day. Money typically reaches your NRE/NRO account within 2-3 working days.

- Tax Efficiency with ELSS: ELSS funds offer a tax deduction of up to ₹1.5 lakh under Section 80C for NRIs with taxable income in India, making them a tax-smart investment.

- Fully Digital Process: You can invest, track, and redeem completely online. No need to physically travel to India.

- Regulated and Transparent: SEBI strictly regulates all mutual funds in India. Daily NAV disclosures, monthly portfolio statements, and annual audits ensure full transparency.

NRI Mutual Fund Investment: Key Rules to Know in 2026

Before you invest, keep these regulatory and practical rules in mind:

- FEMA Compliance: All NRI investments must comply with FEMA guidelines. Repatriable investments (via NRE) are permitted freely. Non-repatriable investments (via NRO) are limited to USD 1 million per financial year.

- SEBI Registration: Only invest through SEBI-registered platforms, AMCs, and distributors. Verify their registration on the SEBI website before transacting.

- Nomination: Always add a nominee to your mutual fund investments. This simplifies asset transfer in case of unfortunate events.

- Power of Attorney (PoA): If you want someone in India to manage your investments, you can assign a PoA. The PoA holder can transact on your behalf with some restrictions.

- Annual KYC Update: Some fund houses and platforms require periodic KYC re-verification to comply with AML/KYC norms. Keep your documents updated.

- ITR Filing: If your total Indian income (including mutual fund gains after TDS) exceeds the basic exemption limit, you must file an Indian income tax return.

Frequently Asked Questions (FAQs) On Mutual Funds For NRIs

How can NRIs invest in mutual funds through online platforms?

NRIs can invest in Indian mutual funds online through AMC websites, government platforms like MF Utility and MF Central, or third-party apps like Kuvera, Groww, and Zerodha Coin. The process involves completing digital KYC, linking an NRE or NRO bank account, submitting a FATCA/CRS declaration, and then selecting and investing in funds. Most platforms support Video KYC, so you can complete the entire process from abroad without visiting India.

What are the top-rated mutual fund companies offering NRI investment services?

The top-rated AMCs that offer NRI investment services in India are SBI Mutual Fund, ICICI Prudential Mutual Fund, Nippon India Mutual Fund, UTI Mutual Fund, HDFC Mutual Fund, Mirae Asset Mutual Fund, and Axis Mutual Fund. For US- and Canada-based NRIs, SBI MF, Nippon India MF, UTI MF, and ICICI Prudential MF are among the few that accept investments with full FATCA compliance.

What are the documents required for NRIs to invest in mutual funds in India?

NRIs need a valid passport copy, PAN card, NRE or NRO bank account proof (cancelled cheque or statement), overseas address proof (utility bill or driving license from country of residence), a recent passport-size photograph, a completed KYC form, and a FATCA/CRS self-declaration. US and Canada NRIs need to submit additional FATCA documents with W-8BEN forms in some cases.

What are the tax implications for NRIs investing in Indian mutual funds?

NRIs pay capital gains tax on mutual fund profits. Equity fund gains held for more than 1 year attract 10% Long Term Capital Gains (LTCG) tax on gains above ₹1 lakh. Short-term gains (less than 1 year) attract 15%. Debt fund gains are taxed as per income slab (short-term) or at 20% with indexation (long-term, held 3+ years). TDS is deducted at source before redemption proceeds are credited. NRIs can claim DTAA benefits to reduce TDS by submitting Form 10F and a Tax Residency Certificate.

What are the benefits of investing in mutual funds as an NRI?

The main benefits include professional fund management, easy diversification across Indian companies and sectors, the ability to invest via SIP from as low as ₹500/month, full liquidity in open-ended funds, tax savings through ELSS under Section 80C, potential rupee appreciation gains, and a fully digital process from abroad. Indian mutual funds are also strictly regulated by SEBI, ensuring transparency and investor protection.

Can NRIs from the USA and Canada invest in Indian mutual funds?

Yes, but with restrictions. Due to FATCA compliance requirements, many Indian AMCs do not accept investments from US- and Canada-based NRIs. However, SBI Mutual Fund, Nippon India Mutual Fund, UTI Mutual Fund, and ICICI Prudential Mutual Fund accept US/Canada NRI investments with proper FATCA documentation including a W-8BEN declaration.

What is the minimum amount NRIs can invest in Indian mutual funds?

Most mutual funds have a minimum lump sum investment of ₹1,000 to ₹5,000. For SIPs, the minimum is as low as ₹100 to ₹500 per month depending on the fund. Some premium or specialized funds may have higher minimums. There is no upper limit for NRI mutual fund investments, but NRO account repatriation is limited to USD 1 million per financial year.

Is the NRI investment in mutual funds repatriable?

It depends on the account you use. Investments made through an NRE (Non-Resident External) account are fully repatriable, meaning you can transfer your invested amount and returns back to your country of residence without any restrictions. Investments through an NRO (Non-Resident Ordinary) account are non-repatriable above USD 1 million per financial year.

Do NRIs need to file Indian income tax returns for mutual fund investments?

NRIs need to file an Indian income tax return (ITR) if their total Indian income, including mutual fund gains after TDS, exceeds the basic exemption limit (₹2.5 lakh for individuals below 60 years). Even if TDS has been deducted, filing an ITR lets you claim refunds for excess TDS or set off capital gains against eligible deductions.

The Bottom Line

Mutual funds for NRIs in India offer a powerful, flexible, and regulated way to grow your wealth in one of the world’s fastest-growing economies. Whether you want to build a retirement corpus, save taxes, or simply keep your financial roots in India strong, the Indian mutual fund market has an option for every goal and risk appetite.

In 2026, the process has never been more NRI-friendly. Digital KYC, online platforms, Video KYC, and FATCA-compliant portals mean you can start investing in minutes from anywhere in the world. Always verify the SEBI registration of any platform you use, keep your KYC documents updated, consult a SEBI-registered investment advisor for personalized advice, and file your Indian income tax returns if required.

Interesting Reads